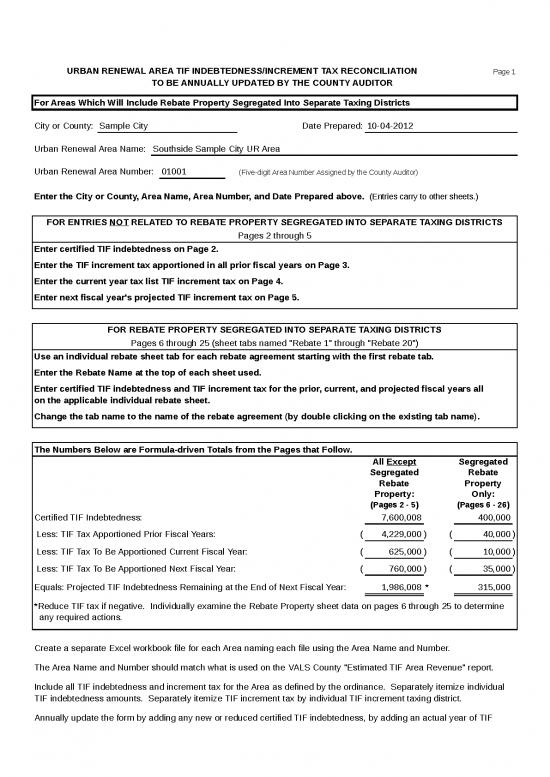

Urban Renewal Area TIF Indebtedness Increment Tax Reconciliation

Tax Increment Financing (TIF) is a public financing method widely used as a subsidy for redevelopment, infrastructure, and other community-improvement projects. In the context of an Urban Renewal Area, TIF allows local governments to capture the future property tax gains from real estate developments within a designated district to pay for the initial infrastructure improvements that stimulated that development.

Understanding the Mechanism

When an Urban Renewal Area is established, the local government sets a "base value" for the property within that district. As the area is redeveloped and property values rise, the tax revenue collected on the original base value continues to flow to the standard taxing entities (such as school districts, cities, and counties). The tax revenue generated from the increase in property valuethe "increment"is diverted into a special TIF fund.

The Role of Indebtedness

The increment is primarily used to pay off the debt incurred by the municipal entity to fund the initial improvements, such as utility extensions, road construction, or land clearance. This debt often takes the form of TIF bonds, tax-exempt notes, or reimbursement agreements with private developers. The "Indebtedness" represents the total financial obligation that the district must service using the captured tax increments.

The Necessity of Tax Reconciliation

TIF Indebtedness Increment Tax Reconciliation is the periodic, systematic process of verifying that the tax increments collected match the actual debt service requirements and contractual obligations of the Urban Renewal Area. This reconciliation serves several critical functions:

- Financial Transparency: It ensures that the funds collected from the increment are being applied strictly to authorized projects and debt obligations as stipulated in the Urban Renewal Plan.

- Fiscal Compliance: It prevents the over-collection or under-collection of tax increments, ensuring that the municipality remains in compliance with state statutes governing TIF districts.

- Sunset Management: Most TIF districts have a fixed lifespan or a maximum debt limit. Reconciliation helps track when the debt is fully retired, triggering the cessation of the TIF and the return of the full tax base to the general tax pool.

1. Calculation of the actual increment received from the county assessor.

2. Comparison of the increment against the scheduled debt service requirements.

3. Adjustment for administrative fees and contractual reimbursement caps.

4. Documentation of any surplus funds or shortfalls in the TIF account.

Challenges in Reconciliation

Reconciliation can be complex due to fluctuations in property tax assessments, varying tax rates from overlapping jurisdictions, and changes in interest rates if the underlying debt carries a variable rate. Additionally, discrepancies may arise if there are tax appeals or abatements that retroactively lower the assessed value within the Urban Renewal Area, potentially reducing the available increment for debt service.

Conclusion

Effective management of an Urban Renewal Area requires rigorous financial oversight. By maintaining an accurate and transparent reconciliation process, local governments can ensure that the TIF mechanism functions effectively as an economic development tool without creating long-term fiscal instability. Proper reconciliation protects the interests of taxpayers and ensures that the financial obligations incurred in the name of urban renewal remain sustainable and focused on their intended outcomes.